Failure to Prevent Fraud Offence: Strict Liability, Offences and Examples (ECCTA 2025)

Introduction

The UK’s new Failure to Prevent Fraud offence, created by the Economic Crime and Corporate Transparency Act 2023, came into force on 1 September 2025.

It places responsibility directly on large organisations to stop fraud being committed by those connected to them. If an employee, agent, subsidiary, or other “associated person” commits fraud for the organisation’s benefit (or a client it provides services to), the organisation itself can be prosecuted.

This is not about organisations being defrauded — it is about organisations benefiting from fraud, whether they knew about it or not.

Penalties include unlimited fines, regulatory investigation, and reputational damage. The offence is already being described by compliance experts as a major shift in UK corporate liability, with the Serious Fraud Office signalling it intends to use the new law from day one.

For a high-level overview, visit our Failure to Prevent Fraud Offence Overview

See also our Failure to Prevent Fraud Offence FAQs and download our full Guide

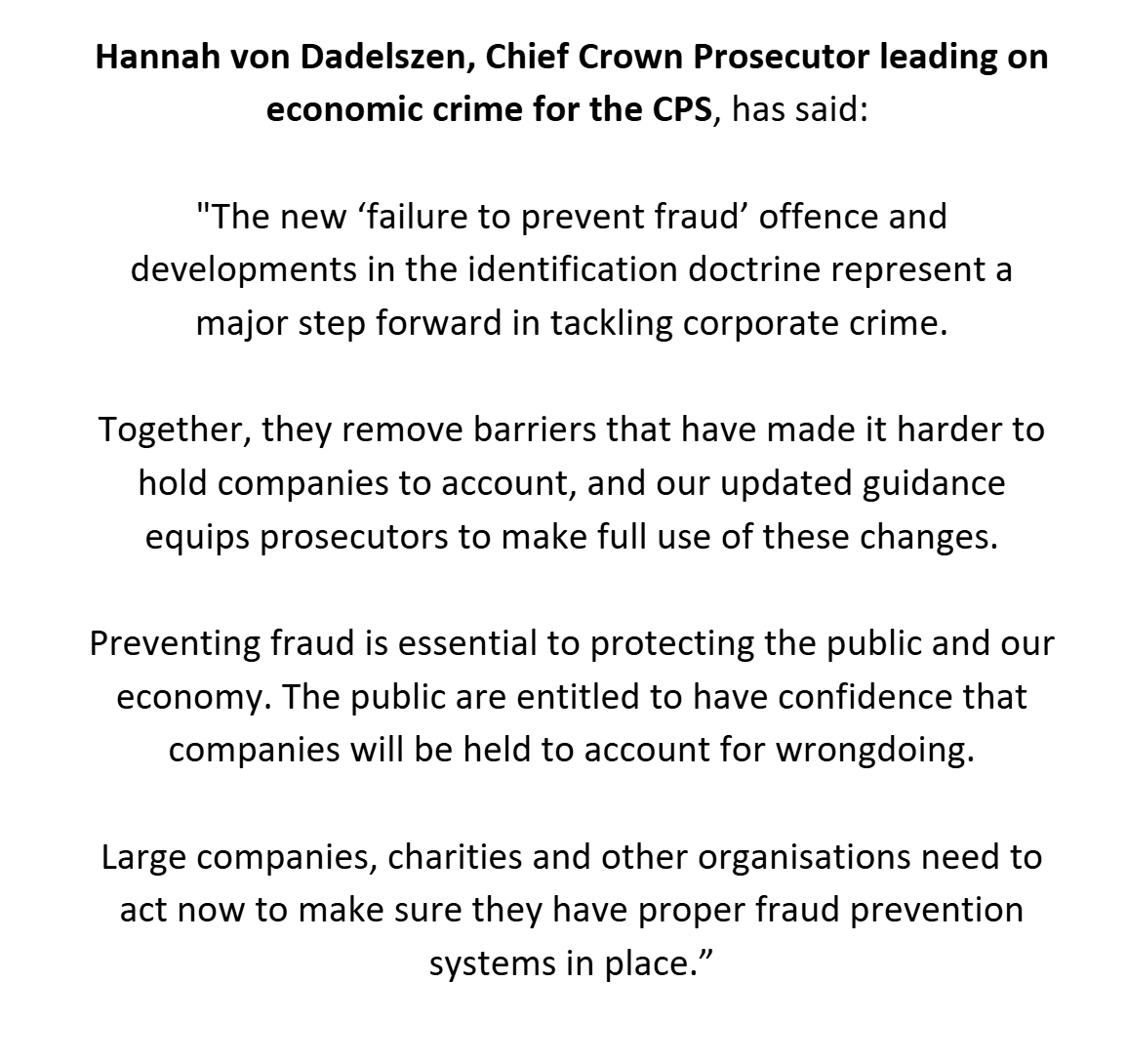

Source: Crown Prosecution Service

What Strict Liability Means for Organisations

The Failure to Prevent Fraud offence is defined as a strict liability offence.

This means:

No need to prove board or senior management knowledge. Prosecutors don’t have to show that directors authorised or were even aware of the fraud.

Liability is automatic if the fraud was committed by an associated person and intended to benefit the organisation (or its client).

The only defence available is to demonstrate that “reasonable prevention procedures” were in place at the time.

Why this matters

It lowers the bar for prosecution: enforcement bodies don’t need to prove intent or awareness at the top.

It removes ignorance as a defence: “we didn’t know” no longer protects an organisation.

It shifts the burden: the organisation must prove it had real, operational prevention measures — not just policies on paper.

Implications for compliance teams

Organisations will need to show they had:

Fraud risk assessments (by unit, geography, third party).

Clear policies and micro-learning delivered to the right teams.

Confidential reporting channels for staff, contractors and partners.

Case management systems with audit trails for investigations.

Third-party oversight to cover suppliers and delivery partners.

Dashboards and trend analysis to brief leadership and show continuous improvement.

In other words, the legislation puts prevention at the heart of compliance. If your organisation cannot evidence its procedures, you will struggle to defend yourself if fraud is uncovered.

imabi gives you the tools and audit trail to evidence those steps.

Fraud offences covered by the law

The Failure to Prevent Fraud offence doesn’t apply to every dishonest act. Instead, it is tied to a defined set of recognised “base fraud offences” in UK law. These are the offences an organisation could be held liable for if committed by an associated person for its benefit.

False accounting (Section 17, Theft Act 1968) – deliberately altering, destroying or falsifying records to hide losses or inflate profits.

False statements by company directors (Section 19, Theft Act 1968) – knowingly providing misleading or false information in company documents or returns.

Fraudulent trading (Section 993, Companies Act 2006) – running a business with intent to defraud creditors, investors, or others.

Fraud Act 2006 Offences

Fraud by false representation (Section 2, Fraud Act 2006) – lying about facts, figures, or credentials to secure a gain or avoid a loss.

Fraud by failing to disclose information (Section 3, Fraud Act 2006) – withholding information you are legally obliged to reveal, to cause a gain or avoid a loss.

Fraud by abuse of position (Section 4, Fraud Act 2006) – exploiting a position of trust, such as a manager misusing company funds or donor money.

Participation in a fraudulent business (Section 9, Fraud Act 2006) – knowingly being involved in running a business set up or conducted to defraud.

Obtaining services dishonestly (Section 11, Fraud Act 2006) – using deception or dishonesty to access services without paying or with improper intent.

Other Offences

Cheating the public revenue (common law) – dishonest conduct to avoid or reduce tax owed to HMRC.

Aiding, abetting, counselling or procuring – assisting or encouraging another person to commit any of the above offences.

If any of these fraud offences are committed for your organisation’s benefit (or for the benefit of a client you provide services to), liability attaches under the law - unless you can prove you had reasonable fraud prevention procedures in place.

imabi gives you the tools and audit trail to evidence those steps.

Corporate and Accounting Offences

Example Scenarios in Practice

To understand how the Failure to Prevent Fraud offence could apply, it helps to look at real-world scenarios.

These examples show the kinds of situations where liability may arise, what benefit the organisation might have gained, and how imabi provides evidence of “reasonable prevention procedures.”

False Financial Reporting

Risk: A finance manager manipulates quarterly accounts to meet earnings targets.

Organisational gain: Protects share price and secures investor funding.

How imabi helps: imabi provides confidential reporting channels for finance staff, audit-ready logs, and policy reminders, giving regulators evidence of active fraud detection measures.

Legal Context: Fraud intended to benefit the organisation triggers liability unless reasonable procedures were in place.

Commercial Organisation Examples

Tax Evasion Schemes

Risk: A senior manager misclassifies costs to reduce corporation tax.

Organisational gain: Improves profitability and short-term cash flow.

How imabi helps: imabi delivers training on financial integrity, provides confidential reporting channels for staff, and stores audit trails showing prevention steps.

Legal Context: Cheating the public revenue (common law).

Supplier Collusion

Risk: A procurement officer certifies substandard goods as compliant to avoid penalties.

Organisational gain: Organisation avoids late-delivery fines and protects client revenue.

How imabi helps: imabi extends oversight to third-party suppliers, enabling reporting of contractor misconduct and centralised monitoring.

Legal Context: Associated person liability — covers employees, agents, and contractors.

Procurement Misrepresentation

Risk: A sales executive falsifies capacity data in a government tender.

Organisational gain: Wins a lucrative contract, securing long-term revenue.

How imabi helps: imabi delivers tender-specific compliance guidance, captures whistleblowing reports, and creates auditable records of preventative training.

Legal Context: Fraud by false representation (Fraud Act 2006, s.2).

Mis-selling of Products

Risk: Bank employees deliberately omit risk disclosures when selling investment products.

Organisational gain: Increases product sales and revenue.

How imabi helps: imabi enables anonymous speak-up channels for pressured staff, tracks misconduct trends, and provides role-specific awareness campaigns.

Legal Context: Fraud by false representation (Fraud Act 2006, s.2).

Donor Reporting Fraud

Risk: Staff exaggerate outcomes in reports to secure repeat funding.

Organisational gain: Maintains donor confidence and future income streams.

How imabi helps: imabi provides role-specific donor reporting training, whistleblowing tools, and audit-ready data trails.

Legal Context: Fraud by abuse of position (Fraud Act 2006, s.4).

Misuse of Restricted Funds

Risk: Executives knowingly reallocate restricted donations to cover central admin costs, while reporting them as properly used.

Organisational gain: Keeps operations solvent and avoids deficit.

How imabi helps: imabi centralises compliance guidance, enables finance staff to flag misuse, and tracks issues for audit.

Legal Context: False accounting (Theft Act 1968, s.17).

Third-Party Partner Fraud

Risk: An overseas partner submits inflated invoices with staff collusion.

Organisational gain: Charity meets donor spending targets, retaining eligibility for future grants.

How imabi helps: imabi provides third-party oversight tools, captures partner-related fraud reports, and analyses anomalies.

Legal Context: Associated person liability — applies to agents and delivery partners.

Charity and Not-for-Profit Examples

Grant Application Misrepresentation

Risk: A programme officer inflates beneficiary numbers in a funding application.

Organisational gain: Secures additional donor grants.

How imabi helps: imabi embeds grant compliance guidance, provides reporting channels for colleagues, and logs actions taken.

Legal Context: Fraud by false representation (Fraud Act 2006, s.2).

Aid Diversion for Organisational Advantage

Risk: A field manager diverts aid to officials to clear customs faster.

Organisational gain: Programmes run smoothly without costly delays.

How imabi helps: imabi offers geo-enabled reporting and escalation tools for field staff, evidencing overseas fraud prevention measures.

Legal Context: Fraud by abuse of position (Fraud Act 2006, s.4).

Reasonable Prevention Procedures – What They Look Like

The Failure to Prevent Fraud offence is unique because the only defence available to an organisation is to prove that it had “reasonable prevention procedures” in place at the time the fraud was committed.

The law doesn’t provide a fixed checklist, but regulators expect organisations to take proportionate, risk-based measures. What is reasonable will depend on the size, sector, and risk profile of the organisation.

Typical elements of a prevention framework include:

Fraud risk assessments – identifying risks across business units, geographies and third parties.

Clear, accessible policies – codes of conduct and fraud policies available to staff and contractors.

Targeted training and micro-learning – delivering awareness modules to the right teams at the right time.

Confidential reporting channels – enabling staff, contractors and partners to report concerns securely and anonymously.

Case management and workflows – documenting investigations, outcomes and escalation processes with a clear audit trail.

Third-party due diligence – onboarding checks, attestations and risk ratings for agents, suppliers and delivery partners.

Ongoing monitoring and alerts – using data to flag emerging risks and running campaigns to reinforce anti-fraud culture.

Board-level oversight – dashboards and trend analysis to brief leadership and demonstrate continuous improvement.

To rely on the “reasonable procedures” defence, organisations must show that prevention measures were not just written down but were actively used, embedded, and monitored.

With imabi, all of these elements are available in one integrated platform, creating a demonstrable audit trail that can be shown to regulators, insurers and investors.

Ready to shore up your defences?

The Failure to Prevent Fraud offence is now in force. Book a demo to see how imabi helps you evidence prevention, reporting and assurance today.